Americo Eagle Premier Final Expense Contracting

For agent use only

Update: We can no longer recommend Americo for final expense agents selling over the phone for the term product or any other product for the reasons listed below.

We were once contracted with Americo and are no longer. We’ll tell the story below (see #4).

Top 5 Reasons To Stay Away From Americo Life

Reason #1: MIB Plan F.

Please Google “MIB Plan F” and know that Americo participates in this.

We received a cease and desist from Americo specifically citing content regarding MIB Plan F. They said “Americo believes that certain statements made related to the use of MIB are untrue and deceptive to anyone who would read this blog post”. While we believe everything to be truthful in our original content, it’s easiest for us to just remove this section.

Reason #2: Non-smoker rates for smokers program

They recently came up with this non-smoker rates for smokers program. On the surface, it sounds great…but no one even knows the process over there.

We couldn’t get a straight answer from Americo on what happens in year 3. Karsten Gebert, the National Sales Director, told us they’ll need to lick a lollipop and send it back. When asked if this would be proactively sent out, we got different responses. A support person said that the agent will be notified and coordinate it, another support person said it will be automatically sent out and another person from Americo said that it’s non a lollipop, it’s a cotton swab.

We tried to get clarity on this for weeks and we couldn’t. Even the agent forums and groups online had differing information. So we couldn’t get behind this non-smoker rates for smokers program.

Reason #3: State license fees

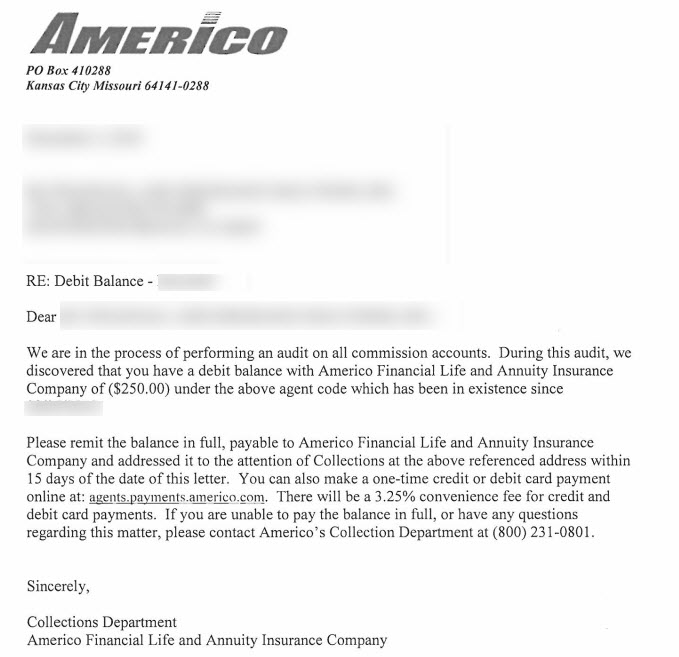

If you’re selling across different states, they’ll charge you state license fees.

We had an agent contract in 5 states and didn’t write any business for 2 months before they started going after him for state license fees of $250:

Simply ridiculous and this isn’t an isolated incident. There were a dozen more agents of ours they did this to.

There’s only a few companies out there that charge for state license fees and Americo is one of them.

Reason #4: Terrible upper management

So here’s the story and I’m sure Americo will see this at some point so I’m going to stick to the facts knowing this will go through legal at some point.

We contracted our BGA with Americo and sent over our proof of production to secure the highest IMO contract available.

2 months in, we did an initial contracting run of 45 agents. We’re just starting to send over cases and getting a feel for Americo and their systems. The National Sales Director, Karsten Gebert, reaches out and says he needs to see more production in order to keep our contract. I said to follow up in a month when we launch Digital Senior Benefits – he agrees.

Another month goes by (entering month 3) and we’re at around 53 contracted agents and starting to write an app/day. At this point we only really notified agents we had Americo as an option and have yet to put our stamp of approval on them because we couldn’t get straight answers about their non-smoker rates for smokers program. So hadn’t done much training unless an agent specifically asked for it. We didn’t hear from Karsten Gebert so we figured we’re pacing just fine.

2 weeks later (3.5 months in) I get a termination letter in the mail for lack of production. No call, no email….nothing. This is after 3 months of having the contract, getting 60 agents contracted and writing daily business with them. So I called and emailed Karsten Gebert for weeks and never heard anything from him – not an email or a returned call.

Speaking with other IMO’s, they said our production was pacing normal and they’ve never heard of a terminated contract 3.5 months in due to lack of production.

I finally get a call from Amy Bock and speak with her and plead our case and ask for a real reason why we’re being terminated. I even recommended going under another IMO and reducing our comp so at least our agents can keep writing them. After putting me off for over a week, she finally emailed me:

This is the last correspondence I’ve had with Americo. They couldn’t even tell me why they won’t accommodate us moving under someone else instead of being direct.

To this day, Americo hasn’t given us a real reason why we were terminated in such a short amount of time and why we couldn’t even be moved under another IMO.

Reason #5: Americo is uncompetitive on price

There’s no reason to write any of their products.

If you want to write Eagle Premier Final Expense because of their underwriting niches, write Royal Neighbors instead. They’re more competitive on pricing, underwriting and have member benefits.

If you loved their HMS series term, even that’s overpriced. Foresters YourTerm has better living benefits and is simplified issue. Need to replace ROP simplified issue term, look at ANICO’s GUL with cash-back options in years 15, 20 and 25 – it has built in living benefits as well. Non med to $250,000 as well.

Bottom Line – Stay Away From Contracting With Americo

You can do better than contracting with Americo Life. The reason you even heard about them in the first place is their high commission levels for both agents AND uplines. Your upline is incentivized financially to write them – that’s why it’s being pushed.

Like we mention above, there’s other more competitive products out there where you don’t risk getting a chargeback from a rescinded policy and also risk leaving your clients uninsured and potentially uninsurable if something happened during the time they owned the policy.